|

The best interest rate on a home loan can vary depending on several factors, including your creditworthiness, the type of loan you're applying for, the lender you choose, and prevailing market conditions. Here are some key factors that can influence the interest rate you might be able to secure:

0 Comments

Eligibility criteria for obtaining a personal loan from a bank can vary depending on the bank's policies, your location, and other factors. However, here are some common eligibility criteria that many banks and financial institutions consider when evaluating personal loan applications: Read More : What Are The Best Personal Loan Interest Rates In India?

The GST (Goods and Services Tax) Calculator is a valuable tool used for various purposes in the context of taxation and financial planning. Here are some of its key uses and more calculators Systematic Investment Plan Calculator Online, Mutual Fund Return Calculator, Net Present Value Calculator, Systematic Withdrawal Plan, FD interest calculator, GST calculator online, Simple Interest Calculator

In today's dynamic financial landscape, acquiring a home loan with less-than-ideal credit may seem like a daunting challenge. At Investkraft we understand that navigating the realm of low-credit home loans requires expert guidance and a comprehensive understanding of the available options. Our mission is to empower you with the knowledge and insights you need to make informed decisions and embark on the path to homeownership, regardless of your credit score. Home Loan Provider, Home Loan Provider in Delhi, Home Loan Eligibility, Home Loan Application  Exploring Your Home Loan Option FHA Loans: A Viable Solution

Federal Housing Administration (FHA) loans are designed to assist individuals with lower credit scores in achieving their dream of owning a home. These loans offer competitive interest rates and require a minimum credit score, making them an accessible option for those with less-than-perfect credit. VA Loans for Veterans If you're a veteran, a VA loan could be the key to unlocking affordable homeownership. These loans come with favorable terms, including competitive interest rates, flexible credit requirements, and the possibility of a zero-down payment. Private Lenders Who Understand In addition to government-backed options, there are private lenders who specialize in working with borrowers with low credit scores. These lenders take a holistic approach, considering your entire financial profile rather than solely relying on your credit score. Navigating the Application Process

While a higher credit score can lead to more favorable loan terms, a larger down payment can also make a significant difference. Saving diligently for a substantial down payment demonstrates your commitment and reduces the lender's risk.

When applying for a low-credit home loan, providing a detailed and compelling application is crucial. Highlight your stable income, employment history, and any efforts you've made to improve your credit.

Consider enlisting the help of a co-signer with a stronger credit history. A co-signer can bolster your application and increase your chances of securing a lower interest rate. Tips and Tricks to Improve Your Chances

Conclusion Securing a home loan with a less-than-ideal credit score is entirely possible with the right approach and expert guidance. Our commitment at investkraft is to equip you with the insights and strategies you need to navigate the complexities of low-credit home loans. We're here to help you take the first steps toward achieving your homeownership dreams, regardless of your credit history. When it comes to home loans in India, there are several types available, each catering to different needs and circumstances. The best type of home loan for you depends on your specific requirements and financial situation. Here are some of the most common types of home loans in India Read More: Need a Personal Loan for Starting an Interior Design Business

Before taking a home loan in India, there are several crucial factors you should consider to ensure a smooth and financially viable borrowing experience. Here are some essential things to keep in mind: Read More

Buying a home is a significant milestone in one's life, but it often involves a substantial financial commitment. Most homebuyers opt for a home loan to finance their dream home. However, before you take the plunge, it's crucial to have a clear understanding of the financial implications, including the Equated Monthly Installments (EMIs) you'll need to pay. Home EMI calculators are powerful tools that can help you estimate your monthly repayments accurately. In this article, we will explore what home EMI calculators are, how they work, and why they are essential for potential homebuyers. What is a Home EMI Calculator A home EMI calculator is an online tool provided by various banks, financial institutions, and real estate websites. Its primary function is to assist homebuyers in determining the monthly EMI amount they would need to pay based on the loan amount, interest rate, and loan tenure. By adjusting these variables, potential borrowers can make informed decisions about their loan and plan their finances accordingly. home loan emi calculator, car loan emi calculator, loan emi calculator, emi calculator car, housing loan emi calculator, emi calculator online, sbi emi calculator, sbi personal loan calculator, emi calculator bike, bike emi calculator, emi calculator india, home loan emi, education loan calculator, education loan calculator emi, online emi calculator, personal loan, emi calculator How Does a Home EMI Calculator Work? Home EMI calculators utilize a simple formula to calculate the Equated Monthly Installment. The formula takes into account the principal amount (loan amount), interest rate, and loan tenure: EMI = [P x R x (1+R)^N] / [(1+R)^N-1 Where: EMI = Equated Monthly Installment P = Principal amount (loan amount) R = Monthly interest rate (annual interest rate divided by 12) N = Loan tenure in months Key Benefits of Using a Home EMI Calculator

Conclusion: A home EMI calculator is an indispensable tool for anyone considering a home loan. It offers valuable insights into the affordability and financial impact of a home loan commitment. By using a home EMI calculator, you can make informed decisions about the loan amount, interest rate, and tenure, ensuring a smooth and stress-free home buying journey. Remember to utilize this tool on reputed financial websites or lender portals to obtain accurate and up-to-date results. Happy house hunting!

Fixed deposits are a popular investment option known for their stability and assured returns. However, there are several myths and misconceptions surrounding fixed deposits and the earned interest. Let's debunk some of the common myths associated with fixed deposits: Read More : Apply for an Instant Personal Loan Online: Convenience at Your Fingertips Myth 1: Fixed Deposits Offer Low Returns Contrary to popular belief, fixed deposits can offer competitive returns. While they may not provide the same level of returns as riskier investments such as stocks, fixed deposits provide a stable and predictable source of income. The interest rates offered on fixed deposits vary depending on the duration and prevailing market conditions. By exploring different banks and financial institutions, investors can find attractive interest rates that align with their investment goals. Myth 2: Fixed Deposits Are Only for the Elderly Another misconception is that fixed deposits are exclusively suitable for elderly individuals or retirees. In reality, fixed deposits are suitable for investors of all ages who prioritize capital preservation, regular income, or short-term financial goals. Fixed deposits provide a secure investment avenue and can be a part of a diversified investment portfolio for individuals across different life stages. Myth 3: Fixed Deposits Have No Risks While fixed deposits are considered low-risk investments, they are not entirely risk-free. One potential risk is inflation. If the interest rate on a fixed deposit is lower than the inflation rate, the purchasing power of the earned interest may decrease over time. Additionally, premature withdrawals may attract penalties or lower interest rates. It's important for investors to carefully assess the terms and conditions of the fixed deposit and consider their financial goals and risk tolerance. Myth 4: Fixed Deposits Lack Flexibility Some individuals believe that fixed deposits lack flexibility, and once the investment is made, it is locked in for the entire duration. However, many financial institutions offer flexibility through premature withdrawal options or the ability to take a loan against the fixed deposit. While these options may come with certain terms and conditions, they provide some degree of liquidity and flexibility for investors. Myth 5: Fixed Deposits Are Outdated In today's fast-paced digital world, some may consider fixed deposits as outdated investment options. However, fixed deposits continue to be relevant and popular due to their simplicity, stability, and guaranteed returns. They serve as a reliable investment tool for risk-averse individuals who prioritize capital preservation and a predictable income stream. Myth 6: Fixed Deposits Require a Large Initial Investment

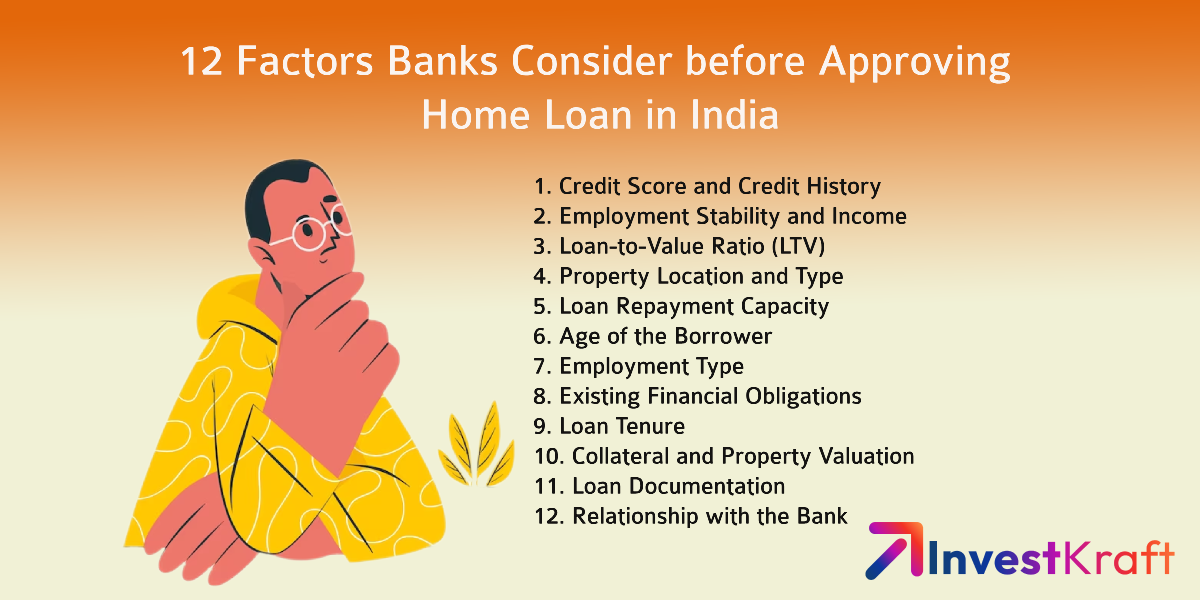

One misconception is that fixed deposits require a significant amount of money to invest. In reality, the minimum investment amount for fixed deposits can vary among financial institutions, and it is often affordable for many investors. This accessibility allows individuals to start small and gradually increase their investments over time. Myth 7: Fixed Deposits Are Tax-Inefficient There is a misconception that fixed deposits are tax-inefficient and result in high tax liabilities. While the interest earned from fixed deposits is subject to taxation, there are tax-saving options available. Investors can explore tax-saving fixed deposits or consider investing in tax-saving instruments such as tax-saving mutual funds or tax-free bonds to mitigate the impact of taxes on their earnings. Myth 8: Fixed Deposits Offer No Additional Benefits Apart from earning interest, fixed deposits can come with additional benefits. Some financial institutions provide the option of periodic interest payouts, allowing investors to receive regular income. Others offer the facility of reinvesting the interest earned, thereby compounding the returns and potentially increasing the overall yield. Additionally, certain fixed deposits can be used as collateral for loans, providing further financial flexibility. Myth 9: Fixed Deposits Are Complex to Understand Fixed deposits are often considered complex financial instruments, deterring some potential investors. However, the concept of fixed deposits is straightforward. Investors deposit a certain amount of money for a specified period at a predetermined interest rate. The terms and conditions, such as interest rates, tenure, and withdrawal options, are clearly outlined by the financial institution. It's crucial for investors to carefully read and understand the terms before investing, but the overall concept is relatively simple. Myth 10: Fixed Deposits Are Prone to Default There is a misconception that fixed deposits are at risk of default by the financial institution. In reality, fixed deposits offered by reputable banks and regulated financial institutions are generally considered safe. It's important to verify the credibility of the institution and check its credit rating before investing. Government-backed deposit insurance schemes in many countries also provide protection to depositors in case of bank failures, further safeguarding their investments. When it comes to purchasing a home in India, many individuals rely on home loans offered by banks. However, before a bank approves a home loan application, they assess various factors to determine the borrower's creditworthiness and the loan's risk profile. In this article, we will discuss the twelve crucial factors that banks consider before approving a home loan in India. Understanding these factors can help prospective homebuyers prepare their loan applications more effectively and increase their chances of loan approval.  Read More: Apply for an Instant Personal Loan Online: Convenience at Your Fingertips Read More: Fixed Deposit Vs Mutual Fund: Which Is Better? 1. Credit Score and Credit History

One of the primary factors banks evaluate is the borrower's credit score and credit history. A credit score reflects an individual's creditworthiness and repayment track record. Banks prefer borrowers with a high credit score, typically above 750, as it indicates a responsible approach towards credit obligations. A clean credit history, devoid of defaults or late payments, significantly enhances the chances of loan approval. 2. Employment Stability and Income Banks assess the stability of the borrower's employment and the consistency of their income. Individuals with a stable job history and regular income are viewed more favorably by banks. The income level is also taken into consideration to determine the borrower's repayment capacity. A higher income can increase the loan eligibility and improve the chances of approval. 3. Loan-to-Value Ratio (LTV) The Loan-to-Value (LTV) ratio is the proportion of the property value that the bank is willing to finance through the home loan. Banks typically finance up to 80% of the property value, while the remaining 20% is expected to be covered by the borrower as a down payment. A lower LTV ratio may increase the chances of loan approval, as it indicates a lower risk for the bank. 4. Property Location and Type The location and type of property being purchased are crucial factors for banks. Properties located in prime areas or those with good market potential are viewed more positively by banks. Additionally, the property's legal status, such as clear title and necessary approvals, is thoroughly evaluated. Banks are cautious about financing properties with legal complications or disputed ownership. 5. Loan Repayment Capacity Banks analyze the borrower's repayment capacity based on their income, existing financial obligations, and monthly expenses. The borrower's Debt-to-Income (DTI) ratio, which compares their monthly debt payments to their monthly income, is a crucial metric. A lower DTI ratio indicates a healthier financial position and increases the likelihood of loan approval. 6. Age of the Borrower The borrower's age is another factor considered by banks. Younger borrowers with a longer working life ahead are often preferred by banks, as it provides a longer repayment period. However, older borrowers may face stricter scrutiny, especially if their loan tenure extends beyond their retirement age. 7. Employment Type Banks assess the borrower's employment type, whether salaried or self-employed. Salaried individuals with a stable job are generally considered less risky. For self-employed individuals, banks evaluate their business stability, income stability, and profitability. A longer business track record and consistent income growth can positively impact the loan approval chances. 8. Existing Financial Obligations The borrower's existing financial obligations, such as ongoing loans or credit card dues, are analyzed by banks. These obligations impact the borrower's overall debt burden and their ability to manage additional loan repayments. Lower existing debt levels and a good repayment history can enhance the chances of loan approval. 9. Loan Tenure The loan tenure, or the duration of the loan, is an important consideration for banks. Longer loan tenures may lead to higher interest costs for the borrower and an increased risk for the bank. Banks often prefer shorter loan tenures as they reduce the overall risk exposure. 10. Collateral and Property Valuation Home loans are secured loans, with the property itself serving as collateral. Banks assess the property's value through independent valuation to ensure it aligns with the loan amount. In case of default, the bank should be able to recover the outstanding loan amount by selling the property. The property's legal and technical aspects are also scrutinized to mitigate any potential risks. 11. Loan Documentation Banks require borrowers to submit various documents, including identity proof, address proof, income proof, property documents, and bank statements. Incomplete or inaccurate documentation can lead to delays or rejection of the loan application. Properly preparing and organizing all the required documents is essential for a smooth loan approval process. 12. Relationship with the Bank Having an existing relationship with the bank, such as holding a savings account or fixed deposit, can be advantageous. Banks may offer preferential interest rates or relaxed eligibility criteria for existing customers. Building a good relationship with the bank can improve the chances of loan approval. Frequently Asked Questions Q: How important is the credit score for a home loan approval? The credit score is highly crucial for a home loan approval. A high credit score indicates good creditworthiness and enhances the chances of loan approval. Banks typically prefer borrowers with a credit score above 750. Q: Can self-employed individuals avail home loans? Yes, self-employed individuals can avail home loans. However, banks evaluate their business stability, income stability, and profitability. Providing proper documentation, including income tax returns and audited financial statements, is essential for self-employed individuals. Q: How does the loan tenure affect the home loan approval process? The loan tenure affects the home loan approval process as longer tenures may lead to higher interest costs for the borrower and increased risk for the bank. Banks often prefer shorter loan tenures to reduce the overall risk exposure. Q: Is it mandatory to provide collateral for a home loan? Yes, home loans are secured loans, and the property itself serves as collateral. The property's value is evaluated by the bank through independent valuation to ensure it aligns with the loan amount. Q: How can I improve my chances of home loan approval? To improve your chances of home loan approval, maintain a good credit score, have a stable employment history, manage your existing financial obligations responsibly, and provide accurate and complete documentation. Building a relationship with the bank can also be beneficial. Q: Can I prepay my home loan before the tenure ends? Yes, most banks allow borrowers to prepay their home loans before the tenure ends. However, prepayment charges or penalties may apply. It's advisable to check the terms and conditions of your loan agreement for prepayment options. Conclusion When applying for a home loan in India, it's crucial to understand the factors that banks consider before approving the loan. By focusing on maintaining a good credit score, demonstrating stable employment and income, managing existing financial obligations responsibly, providing accurate documentation, and choosing a property with clear legal status, prospective homebuyers can improve their chances of loan approval. Remember to conduct thorough research and compare different loan options before finalizing the lender and loan terms. Are you planning to purchase your dream home? Securing a home loan is an essential step towards fulfilling your homeownership aspirations. However, choosing the right home loan requires careful consideration and thorough research. To ensure that you select a home loan that suits your needs and financial situation, it is crucial to follow a comprehensive checklist. In this article, we will guide you through the important factors to consider when choosing a home loan.  Read Also: How to Choose the Right Bank for a Fixed Deposit Investment

Read More: How Does a Mutual Fund Return Value Calculator Work? Assessing Your Home Loan Requirements Before diving into the home loan selection process, start by assessing your specific requirements. Determine the loan amount you need, taking into account the property’s cost, your savings for the down payment, and additional expenses such as registration fees and taxes. Understanding your financial goals and capacity will help you narrow down your choices. Understanding Different Types of Home Loans Familiarize yourself with the different types of home loans available in the market. home loan application, hdfc home loan interest, union bank home loan interest rate, sbi loan interest rate, axis bank home loan, best home loan interest rates. Common options include fixed-rate loans, adjustable-rate loans, government-backed loans, and specialized loans for first-time homebuyers. Each type has its own features, benefits, and eligibility criteria. Evaluate the pros and cons of each type based on your financial situation and preferences. Determining Your Budget and Affordability Assess your budget and determine how much you can afford to borrow. Consider your income, monthly expenses, and any existing financial commitments. Use online calculators to estimate your loan affordability and monthly repayments. It is essential to choose a loan amount that fits comfortably within your budget to avoid future financial stress. Researching and Comparing Lenders Research different lenders and financial institutions to find the ones offering home loans that meet your requirements. Consider factors such as interest rates, loan terms, reputation, customer service, and flexibility in loan repayment. Read customer reviews and seek recommendations from trusted sources to gain insights into the lender’s reliability and responsiveness. Interest Rates and Loan Terms Compare the interest rates offered by different lenders. Even a slight difference in interest rates can significantly impact your overall loan repayment amount. Evaluate the loan terms, including the loan tenure, frequency of repayments, and any penalties for early repayments. Choose a loan with favorable terms that align with your financial goals. Loan Eligibility Criteria Understand the eligibility criteria set by lenders for home loan applicants. Factors such as income, credit score, employment stability, and existing debts play a crucial role in determining your eligibility. Check if you meet the requirements of the lenders you are considering and ensure that you have the necessary documentation to support your application. Down Payment and Loan-to-Value Ratio Consider the down payment requirement and loan-to-value (LTV) ratio set by different lenders. A higher down payment can help you secure better loan terms and reduce the loan amount. Understand the LTV ratio, which represents the loan amount as a percentage of the property’s value, and choose a lender with favorable ratios. Additional Fees and Charges In addition to interest rates, lenders may charge various fees and charges. These can include loan processing fees, valuation fees, legal fees, and administrative charges. Compare the fee structures of different lenders to understand the overall cost of obtaining the loan. Be aware of any hidden fees and factor them into your decision-making process. Pre-Approval Process Consider obtaining pre-approval from your chosen lender before starting your home search. Pre-approval provides an estimate of the loan amount you can borrow based on your financial situation. It gives you a clear budget to work with and enhances your negotiating power when making offers on properties. Loan Documentation Requirements Familiarize yourself with the documentation required for the home loan application process. Common documents include identification proof, income proof, bank statements, tax returns, and property-related documents. Ensure that you have all the necessary documents in order to streamline the application process. Loan Disbursement and Repayment Options Understand how the loan disbursement process works. Some lenders disburse the loan amount in full, while others may disburse it in stages based on the construction progress of the property. Explore the repayment options available, such as equal monthly installments or graduated payment plans, and choose the one that suits your financial situation. Terms and Conditions Thoroughly review the terms and conditions of the home loan agreement before signing. Pay attention to details such as prepayment penalties, late payment charges, and the possibility of refinancing in the future. Ensure that you fully understand your rights and obligations as a borrower. Seek Professional Advice Consider seeking advice from a financial advisor or mortgage broker who specializes in home loans. These professionals can provide personalized guidance based on your specific needs and financial situation. They can help you navigate the complexities of the home loan process and assist in choosing the most suitable loan option. Conclusion Selecting the right home loan is a crucial step towards achieving your dream of homeownership. By following a comprehensive checklist and considering factors such as loan requirements, lender research, interest rates, eligibility criteria, fees, documentation, and professional advice, you can make an informed decision that aligns with your financial goals. Take the time to evaluate your options and choose a home loan that provides you with the necessary financial support while offering favorable terms. FAQs Q: How much down payment should I aim for when applying for a home loan? A: The down payment amount typically depends on the lender’s requirements and the loan program. However, a higher down payment, such as 20% of the property’s value, can help you secure better loan terms and reduce the overall loan amount. Q: Can I apply for a home loan if I have a low credit score? A: While a low credit score can affect your loan eligibility and interest rates, it may still be possible to obtain a home loan. Some lenders offer specialized loan programs for individuals with less-than-perfect credit. It is advisable to explore different lenders and discuss your options with them. Q: What is the maximum loan tenure available for home loans? A: The maximum loan tenure for home loans varies among lenders. It typically ranges from 15 to 30 years, depending on the lender’s policies and the borrower’s age at the time of loan application. Q: Can I switch lenders or refinance my home loan in the future? A: Yes, it is possible to refinance your home loan or switch lenders in the future. However, it is important to review the terms and conditions of your existing loan agreement and consider any associated costs before making such a decision. Q: How long does the home loan approval process usually take? A: The home loan approval process can vary depending on several factors, including the lender’s internal processes and the completeness of your documentation. On average, it can take anywhere from a few weeks to a couple of months. |